Scenarios

Scenarios defines the stress assumptions applied to the portfolio - shocks such as a jump in PAR, mass restructuring, a sector downturn or a deterioration in PD/LGD. Each scenario codifies the shock parameters so they can be applied consistently and repeatably in stress runs.

Workflow

- Create a scenario and name the shock it represents.

- Set the shock parameters (PAR uplift, PD/LGD increase, default migration).

- Define the macro overlay or sector affected if applicable.

- Save the scenario for use in stress runs.

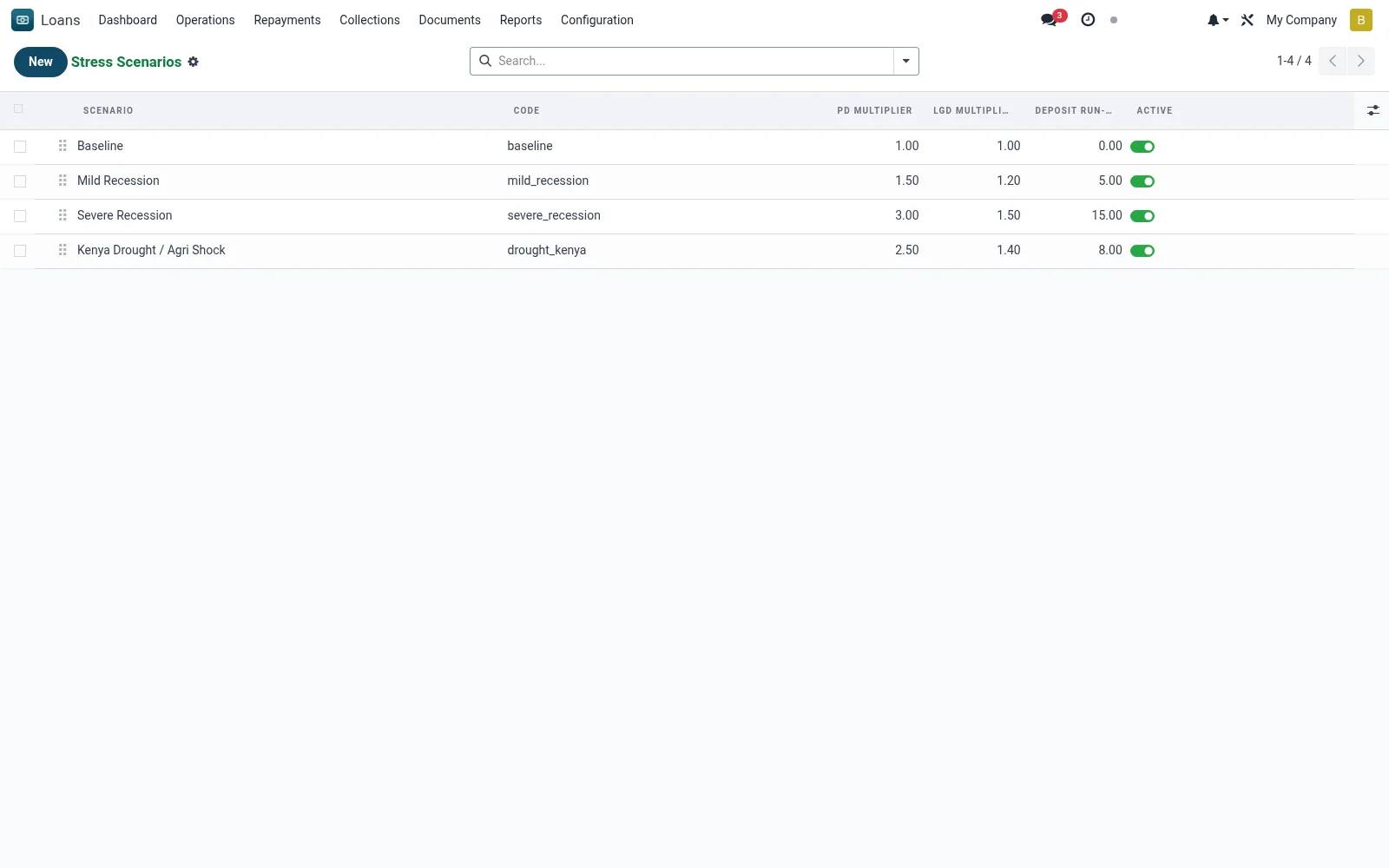

- Maintain a library of baseline, moderate and severe scenarios.

Fields reference

Every field on this screen, drawn from the live data model.

| Field | Type | Required | Description |

|---|---|---|---|

PD Multiplierpd_multiplier | Decimal | — | Multiplier applied to probability of default |

LGD Multiplierlgd_multiplier | Decimal | — | Multiplier applied to loss given default |

Deposit Run-off %deposit_runoff_pct | Decimal | — | Percent of savings withdrawn under stress |

Scenarioname | Text | Yes | Scenario |

Codecode | Text | Yes | Code |

Sequencesequence | Number | — | Sequence |

Activeactive | Yes/No | — | Active |

Descriptiondescription | Long text | — | Description |

Interest Rate Shock %interest_rate_shock | Decimal | — | Interest Rate Shock % |

FX Shock %fx_shock | Decimal | — | FX Shock % |

Notes & rules

- Model: mfi.stress.scenario.

- Parameters: PAR shock, PD/LGD uplift, migration, sector overlay.

- Consumed by Stress Runs.

- Supports ICAAP and supervisory stress expectations.

Was this page helpful?