Scenarios

Scenarios defines reusable stress assumptions such as deposit-run rates, interest-rate shocks, FX moves and asset haircuts, each grouped into a named scenario. These definitions describe how shocks are applied to positions and liquidity when a run is executed. Maintaining a library of scenarios lets the SACCO test mild, moderate and severe conditions consistently.

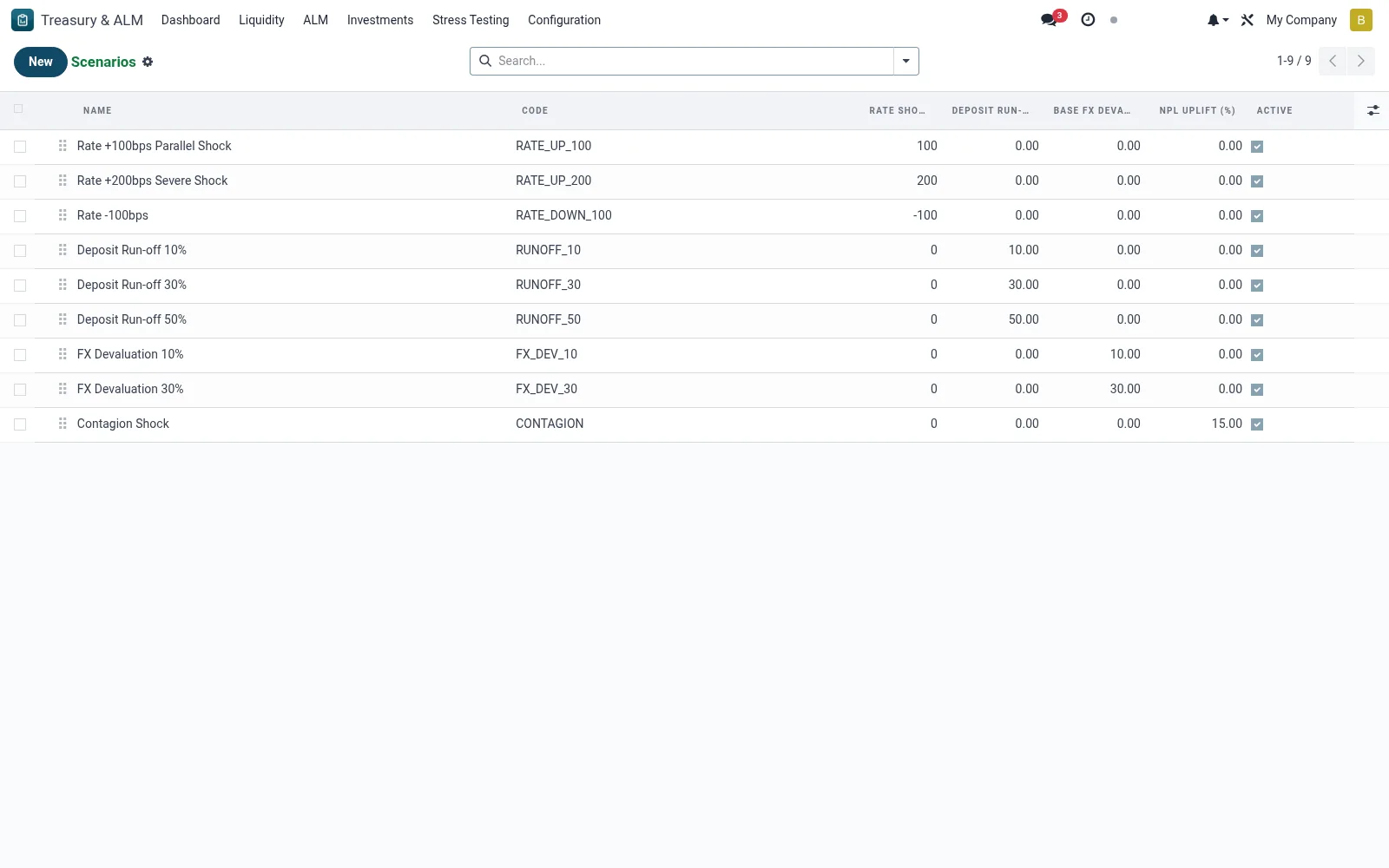

Workflow

- Open Treasury & ALM then Stress Testing then Scenarios.

- Create a scenario and name the stress it represents.

- Set the shock parameters such as deposit outflow, rate move and haircuts.

- Save the scenario so it is available to execute as a run.

- Maintain a graded set spanning mild to severe stress.

Fields reference

Every field on this screen, drawn from the live data model.

| Field | Type | Required | Description |

|---|---|---|---|

Rate Shock (bps)rate_shock_bps | Number | — | +100 = +1% across the curve; -100 = -1% |

Contagion Factorcontagion_factor | Decimal | — | Multiplier applied to inter-bank exposure losses |

Namename | Text | Yes | Name |

Codecode | Text | Yes | Code |

Sequencesequence | Number | — | Sequence |

Activeactive | Yes/No | — | Active |

Descriptiondescription | Long text | — | Description |

Deposit Run-off (%)deposit_runoff_pct | Decimal | — | Deposit Run-off (%) |

Base FX Devaluation (%)fx_devaluation_pct | Decimal | — | Base FX Devaluation (%) |

NPL Uplift (%)npl_uplift_pct | Decimal | — | NPL Uplift (%) |

Companycompany_id | Link → res.company | — | Company |

Notes & rules

- A scenario is a parameter set, not a result; results come from runs.

- Shocks can cover liquidity, interest-rate and FX dimensions together.

- Severity grading supports a structured stress-testing programme.

- Scenarios are reused across multiple reporting dates for comparability.

Was this page helpful?