Macro scenarios — forward-looking overlay

IFRS 9 demands that ECL reflect 'reasonable and supportable' forward-looking information. The macro scenarios page is where that forward-looking lens is built — usually three scenarios (base, upside, downside), each with macro inputs and a probability weight, blended into a single ECL number.

Why macro scenarios exist

Historical default rates tell you what borrowers did in the conditions of the past. IFRS 9 wants ECL to reflect what borrowers will do in the conditions of the future. The bridge between the two is a macro model: a set of macroeconomic factors that explain default behaviour, projected forward under multiple scenarios, with each scenario probability-weighted.

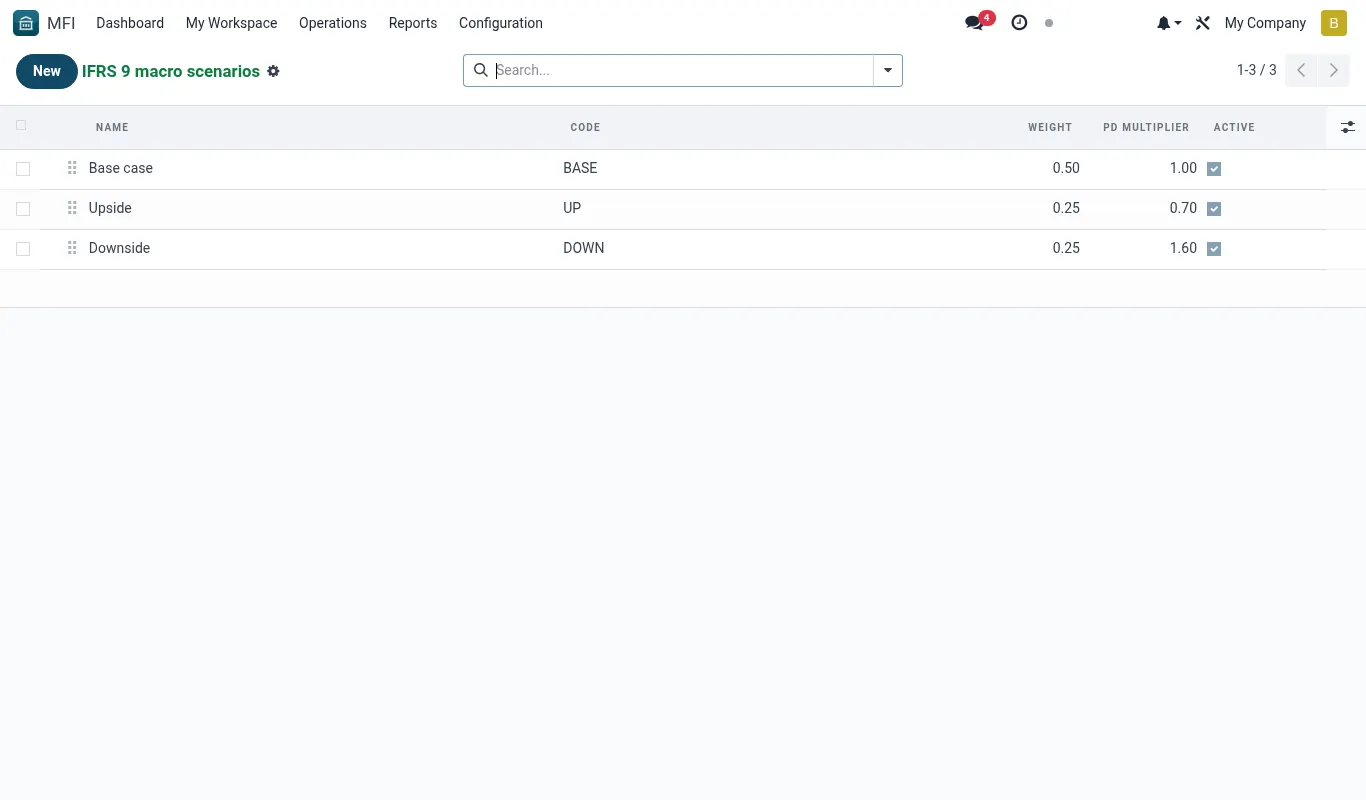

We use three scenarios — a base case (most likely), an upside (better than expected), and a downside (worse than expected). Each scenario adjusts the through-the-cycle PD by a scalar derived from its macro factor projections. The final ECL is the probability-weighted ECL across the three scenarios.

The macro factors we use

Five Kenyan macroeconomic factors drive the PD overlay. They were selected from a longer list after back-testing against the internal default series. Each factor is sourced from a public release and refreshed before each quarter-end.

| Factor | Source | Update frequency | Relevance |

|---|---|---|---|

| Real GDP growth (y/y %) | KNBS Quarterly GDP release | Quarterly | Strong driver for business + SME segments |

| CPI inflation (y/y %) | KNBS Monthly CPI | Monthly | Consumer purchasing power, emergency loan stress |

| KES/USD exchange rate | CBK indicative | Daily | Import-cost shocks for trading SMEs |

| CBR (Central Bank Rate %) | CBK Monetary Policy | Bi-monthly | Funding cost + arrears correlation |

| Long-rains rainfall index | Kenya Met Office | Seasonal (Mar-Jun) | Agriculture segment driver |

How factors become a PD overlay

Each segment has a fitted linear overlay equation that maps macro factor deviations from baseline to a PD multiplier. The equations were fitted on 8 years of macro × default data using a least-squares regression.

The floor and cap prevent the overlay from producing unreasonable numbers when a factor moves outside the calibration range. They are documented in the model documentation and the cap has been hit twice in the last three years (Covid-19 H1 2020 and the 2022 FX shock).

# Example — Business SME segment overlay

# Calibrated coefficients (stored on ifrs9.segment.overlay)

# beta_gdp = -0.45 (1pp lower GDP → +45% PD)

# beta_cpi = +0.12 (1pp higher CPI → +12% PD)

# beta_fx = +0.08 (KES/USD +1% → +8% PD)

# beta_cbr = +0.18 (CBR +1pp → +18% PD)

def pd_multiplier(segment, scenario):

s = scenario.macro_factors # dict of projected values

delta_gdp = s['gdp'] - segment.baseline_gdp

delta_cpi = s['cpi'] - segment.baseline_cpi

delta_fx = (s['fx'] / segment.baseline_fx) - 1.0

delta_cbr = s['cbr'] - segment.baseline_cbr

raw = 1.0 \

+ segment.beta_gdp * delta_gdp \

+ segment.beta_cpi * delta_cpi \

+ segment.beta_fx * delta_fx \

+ segment.beta_cbr * delta_cbr

return max(0.4, min(raw, 2.5)) # floor 0.4×, cap 2.5×Scenario weights

After each scenario produces its own ECL, the three are blended:

Default weights are 50% base / 25% upside / 25% downside. The Risk Committee can shift weights when forward-looking conditions justify it — most commonly raising the downside weight in periods of macroeconomic stress.

ecl_weighted = w_base * ecl_base + w_upside * ecl_upside + w_downside * ecl_downside

# w_base + w_upside + w_downside == 1.0Projection horizon

Macro factors are projected over a horizon that covers the longest expected lifetime in the loan book — typically 5 years. Years 1-2 are the 'reasonable and supportable forecast' period (from named institutional forecasts). Years 3-5 revert linearly to the long-term mean.

| Year | Source | Method |

|---|---|---|

| 1-2 | IMF WEO + CBK / Treasury BPS forecast | Direct institutional projection |

| 3 | Linear blend | 75% institutional / 25% long-term mean |

| 4 | Linear blend | 50% / 50% |

| 5+ | Long-term mean | Through-the-cycle baseline |

What you see on the screen

IFRS 9 → Configuration → Scenarios lists the current scenario set. The screenshot shows base / upside / downside with their respective weights, macro factor inputs, and a 'last approved' stamp. Editing requires Risk Manager privileges; posting requires CFO sign-off.

Worked scenarios

Scenario — Pandemic-style downside shock — Risk Committee raises downside weight

| Character | Role |

|---|---|

| Kimani Mwangi | Risk Manager |

| Florence Achieng | CFO |

| Peter Otieno | Board Risk Committee Chair |

| Mary Mutua | Head of Credit |

Timeline

- Mar 18: Risk Committee meets ad-hoc. Reviews global infection trajectory and 2020 default playbook. (Minute item 1)

- Mar 18: Committee decides: downside weight 25% → 40%, base 50% → 45%, upside 25% → 15%. Downside scenario macro factors adjusted: GDP -3pp, CPI +2pp, KES/USD +8%. (Minute item 2)

- Mar 19, 10:00: Kimani opens IFRS 9 → Scenarios. Edits the downside scenario in draft. Updates the three macro factors and saves. (ifrs9.scenario state=draft)

- Mar 19, 11:30: Kimani edits the weights. System refuses — weights must sum to 100%. Re-checks: 45+15+40 = 100. Saves. (Validation OK)

- Mar 19, 14:00: Kimani attaches the minute extract as supporting evidence. (ir.attachment linked)

- Mar 20, 09:00: Florence reviews and approves. CFO sign-off captured. (ifrs9.scenario state=approved, effective Mar 31)

- Mar 31, 23:59: Quarter-end snapshot. Q1 run starts. (ifrs9.run state=snapshotted)

- Apr 2: ECL computed. Base scenario ECL: KES 9.1M. Downside scenario ECL: KES 24.6M. Weighted: KES 14.2M (vs Q4 KES 9.8M). (state=computed)

- Apr 4: Florence walks board through the ECL bridge: +KES 3.4M from downside weight change, +KES 1.0M from macro factor stress. (Audit pack section 4)

Outcome — Forward-looking provision built ahead of the actual default deterioration; board comfortable; auditor satisfied with the documentation trail.

Reference

ifrs9.scenario fields

| Field | Type | Notes |

|---|---|---|

| name | Char | e.g. 'Base — Q4 2026' |

| scenario_type | Selection | base | upside | downside | custom |

| weight | Float | Probability weight 0.0 – 1.0 |

| effective_from | Date | First run this applies to |

| effective_to | Date | Last run this applies to |

| macro_factors_json | Text(JSON) | Year-by-year projections of each factor |

| approved_by | Many2one(res.users) | CFO required |

| approval_evidence_ids | One2many(ir.attachment) | Minutes, MoUs, reports |

Default shipped scenario set

| Scenario | Weight | GDP y1 | CPI y1 | KES/USD | CBR |

|---|---|---|---|---|---|

| Base | 50% | 5.0% | 6.5% | 130 | 10.50% |

| Upside | 25% | 6.2% | 5.0% | 125 | 9.50% |

| Downside | 25% | 2.8% | 9.0% | 142 | 12.50% |

Troubleshooting

| Symptom | Likely cause | Fix |

|---|---|---|

| Cannot save scenario — error 'weights must sum to 1.0'. | Decimal rounding (e.g. three rows of 0.333 = 0.999). | Adjust one weight to absorb the rounding (e.g. base 0.34, upside 0.33, downside 0.33). Better: use weights that sum exactly (0.5 / 0.25 / 0.25). |

| All three scenarios produce identical ECL. | Macro factor projections are identical across scenarios, usually because someone copied the base without editing. | Open the upside and downside scenarios and ensure macro_factors_json differs from base. The validator should warn — check that the warning was not dismissed. |

| PD overlay multiplier is hitting the cap (2.5×) on most segments. | Downside scenario macro factors set unreasonably extreme. | Sense-check downside: should be a plausible bad case, not Armageddon. The cap is a safety net, not a target. Refer to peer benchmarks or historical 2008/2020 reference set. |

| Auditor asks 'why was the upside weight 25% in a clearly improving environment?' | Weights have not been refreshed during a multi-quarter expansion. | Take a weight-review proposal to Risk Committee. Document the rationale for keeping vs changing. Symmetry isn't required — weights should reflect the genuine distribution of forward outcomes. |

| Macro factor source unavailable (e.g. KNBS release delayed). | External release missed deadline. | Use the most recent available release and document the data lag in the audit pack. Do not delay the run — IFRS 9 explicitly allows reasonable approximation when current data is unavailable. |